In the personal loan industry, few topics stir as much debate as payday loans. These short-term, high-interest loans have been a financial lifeline for many middle-class individuals facing unexpected financial challenges. Yet, recent strides in artificial intelligence (AI) and evolving regulations are poised to redefine the landscape of personal loans, payday loans, and installment loans, Read More

Overview of the article: The article explores the emergence of installment loans as a beneficial alternative for middle-class employees seeking financial flexibility. Installment loans provide structured repayment plans and have become a vital resource for individuals requiring funds for various purposes. The integration of technology, particularly artificial intelligence (AI), in the lending sector has significantly Read More

Get the Funds You Need in a Flash: The Ultimate Guide to Payday Loans Unlock the secret to instant financial relief! Unlike traditional loans that drag you through a maze of paperwork and nerve-wracking credit checks, payday loans zoom right past the red tape and deliver much-needed funds straight into your hands. Embrace the thrill Read More

Installment loans are a useful financial tool for unexpected expenses or large purchases. These loans provide borrowers with a lump sum of money that is repaid through regular monthly installments over a fixed period.Traditionally, securing an installment loan involved physically visiting a lending institution with a lengthy application process. Yet, thanks to the internet’s emergence, Read More

Understanding Online Installment Loans for Individuals with Bad Credit An online installment loan is a viable financial solution, particularly for individuals grappling with a less-than-ideal credit history. Unlike other loan types, an installment loan is repaid in fixed, equal payments spread across a predetermined period. This structure allows borrowers to access the full loan amount Read More

Installment loans can be a helpful way to finance a major purchase, consolidate debt, or cover unexpected expenses quickly. Most Online installment loan lenders generally deposit the funds (money) into your bank account within one working day. The quick turnaround from approval to funding is what makes online installment loans a popular choice. What is Read More

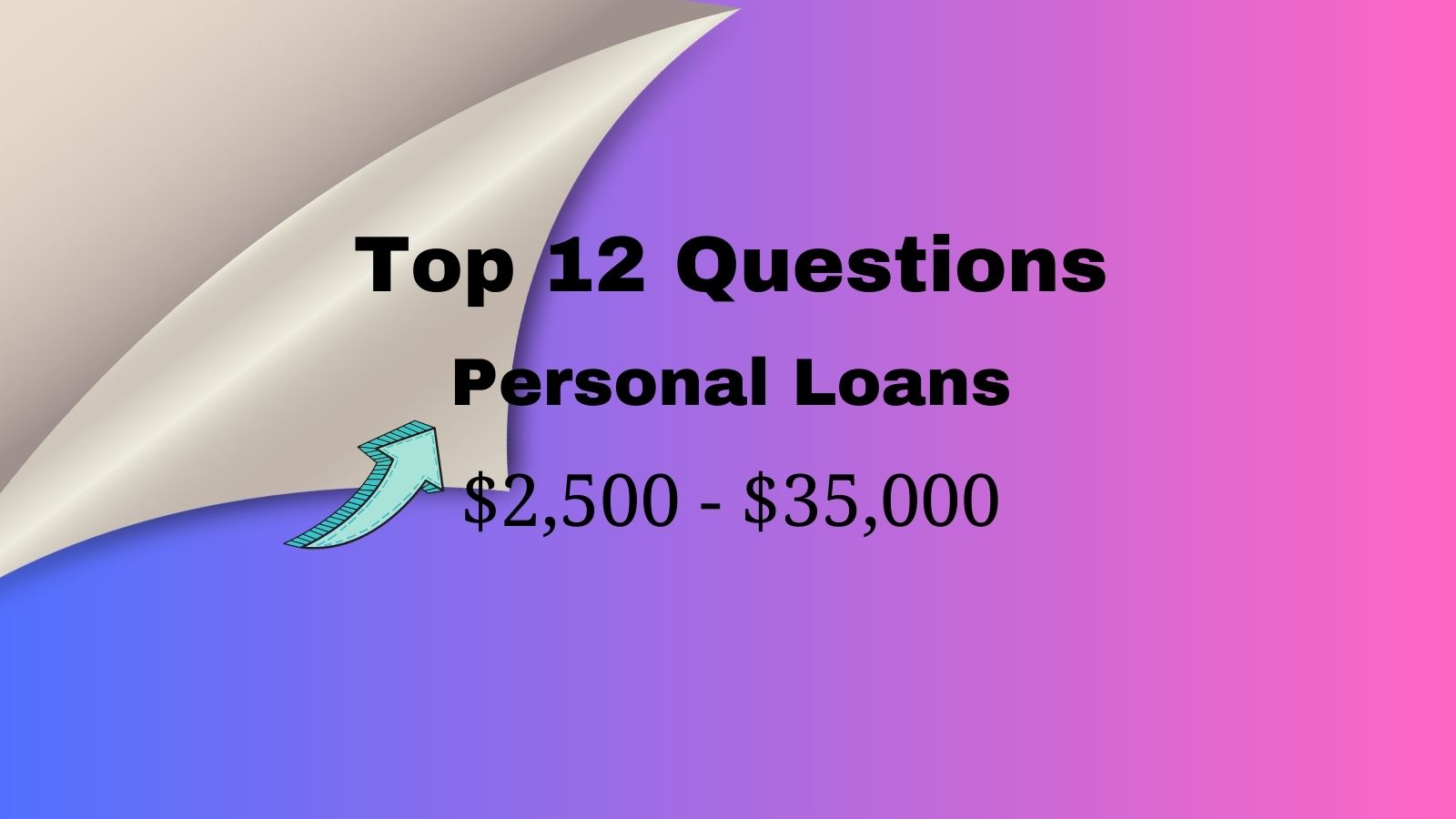

In this article, we will delve into the top 12 questions surrounding personal loans from $2,500 to $35,00. If you’re ready to learn more about these loans and make informed decisions about your financial future, let’s get started! What is a personal loan? A personal loan is a type of loan that individuals can borrow Read More

When in need of quick money, personal loans, and installment loans are two popular choices that provide a simple application process and financial flexibility. Before applying for a loan, it’s crucial to understand the differences, benefits, and drawbacks of the loan types available. This post will provide an in-depth overview of personal loans, installment loans, Read More

What is a bad credit installment loan Installment loans for bad credit are secured or unsecured loans specifically designed for consumers with poor or low credit scores. Having bad credit means having a history of financial difficulties, such as late payments, defaults, or high levels of debt, which has negatively affected your creditworthiness in the Read More