In today’s unpredictable economic climate, finding fast and reliable ways to access money can be a game changer. Whether you’re facing an unexpected medical bill, car repair, or need cash for a personal matter, quick cash loans or personal loans offer a potential solution for millions of Americans navigating short-term financial challenges. Understanding Personal Loans: Read More

You need quick money for an emergency expense or a new purchase, but you’re unsure which option to choose. This article will help you understand the differences, advantages, and disadvantages between personal loans and credit cards, helping you to make better decisions regardless of your credit. Understanding Personal Loans and Credit Cards What is a Read More

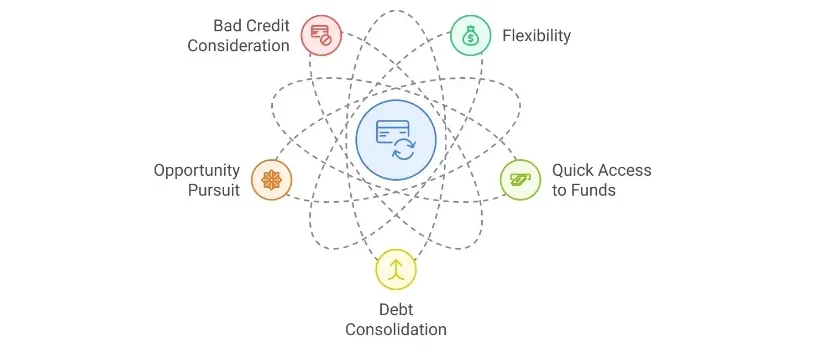

Personal loans offer flexible financial solutions for working professionals seeking quick access to funds. Whether, you’re managing unexpected expenses, consolidating debt, or pursuing business opportunities, personal loans provide the means to navigate complex financial situations—even if you have bad credit. What Are Personal Loans? Fast Cash Solutions Explained Personal loans are simple. The borrowed money Read More

Are you in need of financial assistance but hesitant due to bad credit? Let’s debunk some common myths surrounding personal loans for bad credit to help you make informed decisions. Understanding the Basics, Benefits, and Drawbacks of Personal Loans Whether you are looking to consolidate debt, finance a large purchase, or cover unexpected expenses, personal Read More

Looking for a personal loan? You’re in the right place. This comprehensive guide covers everything you need to know about securing a personal loan with competitive rates – even if your credit isn’t perfect. Key Takeaways How Much Can You Borrow? Personal loan amounts vary by lender and your qualifications: Good to Excellent Credit (670+) Read More